Xpel 2022 Earnings Review

Why Declining New Vehicle Prices Are Good For Xpel

Xpel Inc (NASDAQ: XPEL)

Xpel reported Q4 and full-year 2022 results on February 28, 2023, before the market open. The highlights were as follows:

The results missed analyst expectations. Revenue came in at $78.5 million vs $81.4 estimated and EPS came in at $0.30 vs $0.44 estimated. I was not expecting this miss, as all indications I observed were pointing to at least a meet. Part of the miss was due to canceled China orders to the magnitude of $3.5 million in revenue. There were also some unexpected one-time expenses, including a $0.4 million inventory write-off, $0.3 million in SG&A severance costs, and $0.4 million in compensation expenses from a previous acquisition. As a result, the stock dropped from the high $70s to the mid $60s. Given the stock had run up into the earnings report significantly, I am not surprised by the move back into the $60-70 range that Xpel’s stock price has seemingly been stuck at for quite some time.

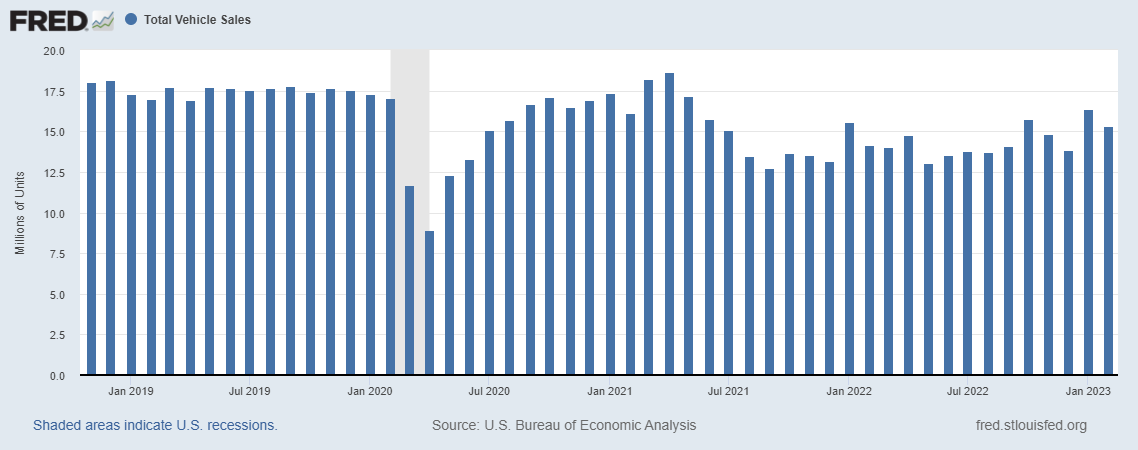

Despite the headwinds in Q4, there were also some positives that I think investors would be keen to take note of. First, US sales were a bright spot this quarter. Xpel’s largest region by revenue, the United States, managed to grow by 31.6% in the quarter. I believe this indicates at least some recovery in the US auto market which has struggled with supply shortages since 2021, countering the bear case that auto sales are getting worse due to a weaker economy. St Louis Fed Total Vehicle Sales seems to suggest that vehicle sales have recovered somewhat, but still remain well below 2019 (pre-pandemic) levels. Of course, the other factor at play here is interest rates, which have also increased above 2019 levels, making it more expensive to finance a vehicle. Despite what you may have seen on FinTwit, interest rates appear to have had minimal effect on new car sales thus far. It appears backlogged orders from supply shortages continue to counteract any negative impact on vehicle sales from increased interest rates.

So absent the challenges in China, most of our other regions had solid quarters. As I mentioned, the U.S. market, which is our largest market, continues to be a bright spot. Revenue grew 31.6% in the quarter to $47.6 million. New car inventory continues to improve, and it remains to be seen the ultimate impact of higher interest rates will be on new car sales, but new car buyers seem to still be resilient at this point, most likely because of pent-up demand.

-Ryan Pape, Xpel Q4/FY 2022 Earnings Call

Another bright spot was guidance, with CEO Ryan Pape suggesting they expect 20-25% growth in revenue in 2023 over 2022. That puts them at $390-400 million of sales for 2023. They also suggested they’d exit 2023 at around a 42% gross profit margin (I’d estimate GPM at 40.5-41.0% for the full year). Xpel expects to see China recover in 2023 after sales fell from $46 million in 2021 to around $34 million in 2022. China will be a key area of focus for Xpel in 2023 and the company will ramp up investment there considerably. Again, this was discussed on the call:

So all that said, I think there's a lot to be positive about regarding the China market. Removing the uncertainty of these restrictions is good news as we see it and our distributor is equally positive in their outlook. As an example, they'll now be hosting their large dealer conference this spring. Our team will be in attendance for, and like ours in the U.S., these conferences are historically well attended and important, and have not been held in a meaningful way since COVID started.

It's been difficult for us in conjunction with the distributor to decide when is the right time to invest further in the market up to now. We've had plans to expand our corporate team into China to better support the distributor, to get us better market intelligence, to support the car dealership, and [indiscernible] groups and our OEM relationships, which are asking us about China.

But with the uncertainty over the past several years, we not move forward on those plans, but we plan to now. We've also held off on product introductions in China like our architectural film in its entirety for similar reasons, uncertainty that prevented our distributor from hiring additional staff, from taking on additional inventory, things that you just were unwilling or was unwise to do under the circumstances, but we do plan to execute on those in 2023.

So overall, I'm encouraged about our opportunities here for China in 2023 and beyond, and about our team's ability to reengage the travel to support the operation as we've always done. I plan to visit as soon as practical, and I think we can use this as a great opportunity to go much deeper on the current state of the market and make sure we're providing the distributor and all of the dealers in China what they need.

-Ryan Pape, Xpel Q4/FY 2022 Earnings Call

Finally, I’d like to emphasize something about Xpel that I think most casual investors simply don’t understand. One bear case I’ve heard lately is that as supply shortages are solved and new car prices come down, Xpel’s sales will suffer, with the theory being that the cost of PPF (paint-protection film) as a percentage of the total vehicle price increases, making it more difficult for the customer to purchase.

I believe the exact opposite is far more likely to occur, and that declining new vehicle prices may in fact be a positive for Xpel for two key reasons. The first is that when new vehicle prices are high and rising, dealers are making close to 100% incremental gross margins on the increase in price. This means the dealer (or OEM in some cases) captures the excess profits and has little incentive to push customers to purchase lower gross margin third-party products such as paint protection film. Fortunately for us Xpel shareholders, automobiles are an extremely competitive market and these excess profits WILL be competed away, leaving dealers with no choice but to reduce vehicle prices and once again look to third-party or aftermarket products to increase sales & gross profits. Ryan Pape has discussed this dynamic on the last two conference calls:

And we continue to see our new car dealerships trading down what is a 100% margin, market price adjustment to more tangible products such as ours. And as a result, we've seen some of the highest revenue from dealership services we've ever seen in January and February of this year, which is not always the strongest months of the year. So that's good news.

-Ryan Pape, Q4/FY 2022 Earnings Call

The second reason I believe declining new vehicle prices are good for Xpel is that, all else equal, a customer with the same amount of money to spend on a vehicle can now buy the vehicle plus a PPF package, instead of just the vehicle. For example, if a customer has $50k to spend and a Tesla costs $50k, they will buy the Tesla for $50k. If, however, the Tesla costs $45k, the customer still has that $50k to spend and can then opt into third-party options and accessories like PPF for an additional $5k.

Of course, the counterargument is that the economy may do poorly and thus the customer no longer has the $50k to spend, but I believe this is a completely separate argument. The economic argument is about DEMAND for new vehicles, while the vehicle pricing has much more to do with the SUPPLY of new vehicles. I recognize that it may very well be the case that demand for new vehicles declines in 2023 (for which there has been no evidence yet) due to a weaker economy and that this could very well impact Xpel. I just think it’s important to distinguish the demand side of the equation separately from the supply side.

I plan on putting out a piece covering Xpel’s numbers in more depth, but the simple back-of-the-envelope math, for now, is as follows. At the guidance midpoint of $395 million of revenue for 2023 and at a 41.0% gross margin, Xpel would produce $162 million of gross profit. They mentioned on the call that SG&A expenses should come in at around 22% of revenue (down from 22.7% in 2022 but up significantly from 19.3% in 2019), costing $87 million. That leaves 75 million of EBIT. Adding back depreciation and amortization at 2% of revenue (approximately the historical amount for Xpel) would put EBITDA at around $83 million. Taxes likely take off $15-16 million on that EBIT number, with interest expense and foreign currency exchange impact taking a few million more. That puts Xpel’s net income at around $55 million for 2023 or right around $2.00 per share.

$2.00 per share was my original estimate back in 2021 for what Xpel could have done in 2022. I still believe they would have been close to this number had vehicle shortages not occurred, and Q3 2022 was proof of this when the company achieved $0.48 of EPS that quarter. Nonetheless, Xpel missed this estimate considerably by producing just $1.50 of EPS in 2022. Ultimately I was right on gross margins, but Xpel spent more on SG&A than I anticipated. It appears 22% of revenue is the new number to model for Xpel’s SG&A expenses going forward, and it remains to be seen whether the 18% number they’ve suggested in the past is still a longer-term target.

Ultimately this sets Xpel back about 1 year in terms of earnings potential from some of my previous estimates. In the long run, I don’t believe this is all that big of a deal. This likely will not matter in a couple of years, much less 5 years from now. But I must admit it is not particularly fun in the shorter term.

At $63 per share using the above numbers, Xpel trades at a Market Cap of $1.74 billion or an Enterprise Value of around $1.72 billion. This would put its EV/EBIT multiple at 22.9, P/E at 31.5, and EV/EBITDA at 21. While these aren’t exactly ultra-cheap multiples, they’re also not particularly high for a 25% organic growth high ROIIC company. If you go out a few more years, I believe the stock begins to look quite attractive today should it trade under $60 per share, but I’ll go into this in more depth in my next piece.

Disclosure: I’m long XPEL.

Disclaimer: This post and all Uncommon Profit posts are not financial advice in any way and should not be taken as such. All articles, including this one, and all information within Uncommon Profits is for educational and informational purposes only. I receive no direct compensation from any company covered. I will profit in the event the share price of these companies increases. Although I make an effort to update readers when possible, I may choose to buy or sell at any time with no obligation to update or notify readers. Consult a professional financial advisor before making any investment decisions.

Thumbnail Image courtesy of Bailey Alexander

Great work! Fellow buyside analyst here. I'd love to talk more about XPEL if you find time. My email is johnthomasgraass@gmail.com. Thank you

Sounds like a good business, but I can’t seem to rationalize the valuation.