XPEL: Now At The Biggest Inflection Point In 4 Years

For patient investors, Xpel still has significant upside.

It’s once again time to take a look at Xpel Inc XPEL 0.00%↑. I haven’t updated readers here in over a year, despite some pretty significant price action in the last 6-7 months (spoiler alert: the fundamental long case has not changed in my opinion).

A quick update for readers wondering where I’ve been - I passed CFA Level 1 last August and am now scheduled to take CFA Level 2 in late May. As such, I’m in the final stages of preparation. After that, I expect to post more on here for a few months before starting on CFA Level 3 in 2025 (assuming I pass L2 in May).

Going forward with this newsletter, my goal is to provide differentiated analysis, asking questions like ‘how’ and ‘why’, rather than ‘what’. I don’t simply want to write a summarized version of a company’s 10-K but rather provide something more unique.

This newsletter is currently free. If you’d still like to support it financially, you can Buy Me A Coffee as a one-time tip here (USD):

The rest of this piece is in bullet form, which I think maximizes the value delivered in the least amount of time for readers while also reducing the time it takes me to write about something. I may continue to experiment with formats like this in the future.

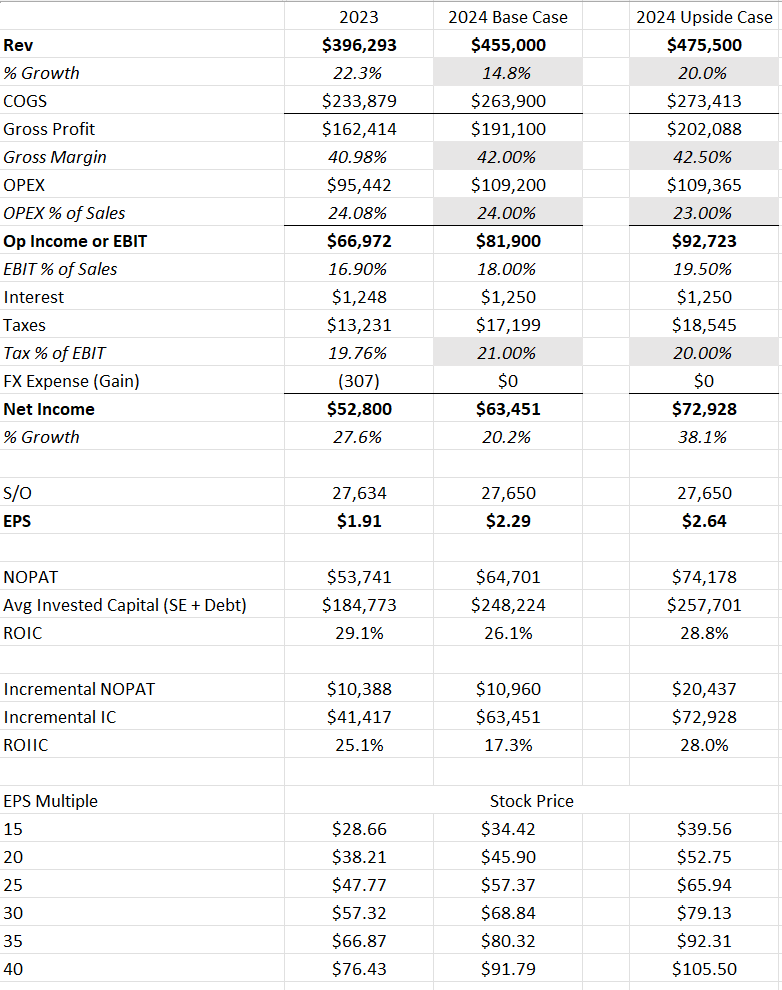

Analyst estimates have shifted from too high to too low. Analyst consensus estimates now have Xpel growing revenue just 11.3% in 2024 vs management’s own 15% guidance. I believe revenue could come in higher than management’s guidance given management’s historically slightly conservative approach to guidance. Analysts have also priced in little to no operating leverage with 11.5% EPS growth resulting in $2.13 of EPS. My low end estimate is closer to $2.29, and as high as $2.64 on the high end (more on this below).

Operating expenses are about to inflect lower as a percentage of sales. This will drive a return to significant operating leverage and considerably improved profitability. This comes after a couple of years of ramping headcount to support future global growth across the business. Now that Xpel has built out the personnel, they can focus on growing the business in new areas (marine PPF, Europe, window film, etc.).

Free cash flow is about to inflect higher as working capital and inventory come under control after multiple years of investment and bloated inventory. This inventory build was due to Xpel building a buffer to counteract potential COVID-related supply chain shortages. I believe this move won Xpel’s installers substantial market share in 2021 and 2022 as there were no other options for consumers when other brands simply ran out of film. This market share is likely retained as evidenced by 2023 financial figures, and 2024 is likely the year Xpel investors finally realize the benefits through the cash flow statement.

The above two points illustrate an under-discussed inflection point in Xpel’s business of once again returning to a combination of further growth + margin expansion.

Management has repeatedly stated that further gross margin expansion is possible. I see a path to 45% gross margins longer term.

“So nothing's changed in terms of our outlook related to the opportunities for that gross margin expansion. We still expect to close the year at/or near 42% gross margin and still expect our gross margin profile to continue to expand in 2024 and then beyond.”

- Ryan Pape, CEO, Q3 2023 Earnings Conference Call

“We've got a number of products we sell in China as an example that have varying margin profiles, so we felt that our expectation is to be back up in the 40% plus for Q1 and then throughout next year. I was happy with the performance in aggregate, even though it was a little bit choppy, as I mentioned, we grew gross margin by 160 basis points. We will build on that. And we still believe that we'll gradually increase our gross margin going forward, kind of ignoring the choppiness of the distribution business. We have room to continue to improve that overall profile like we've been talking about.”

- Ryan Pape, CEO, Q4 2023 Earnings Conference Call

Organic growth opportunities remain substantial, particularly internationally. Regions such as Europe, China, the Middle East (Saudi Arabia), India, Japan, Korea, and Australia remain severely underpenetrated and are key near-term focus areas for Xpel. Further opportunities exist in underpenetrated emerging markets with strong car cultures such as Brazil, Mexico, and Indonesia.

Xpel’s software is objectively moving further ahead of the competition from a ‘nice-to-have pattern software’ to a one-of-a-kind, mission-critical, and fully integrated suite of business management solutions.

This is directly contradictory to the blatantly false and highly manipulative bear narrative that competitors are “catching up” on software.

3M, Eastman, and other no-name software competitors simply do not have the resources or expertise to build this software for installers. Existing CRM software options are too expensive and lack the customizability or feature set to adequately meet the unique needs of Xpel installers. Xpel, on the other hand, has a CEO with a computer science degree (Yes, Ryan Pape is a software developer in addition to being an all-time great operator). I believe competing installers from other PPF brands who do not have access to this software will face a cost disadvantage and ultimately be left in the dust operationally.

Xpel’s Acquisitive pipeline remains strong and large. Xpel often acts as the sole buyer providing an exit for individual shops upon owner retirement. Xpel can make these acquisitions at accretive multiples and easily tuck these acquisitions into existing operations, streamlining administrative work and resulting in small but considerable synergies.

Xpel will be producing enough cash going forward to participate in larger acquisitions. The last major deal Xpel did was in 2021 when they acquired Protex for $30M, adding approximately $6M of EBITDA immediately. Management has stated they’re looking at $25-50M acquisitions. Such acquisitions could materially move the needle for Xpel and are not currently built into forward estimates. Xpel can easily finance these acquisitions through debt and internally generated cash flow.

Given historical acquisition multiples, I estimate that a $50M acquisition would likely immediately add $6-12M of incremental EBITDA for Xpel.

“First, we're looking to expand our distribution to other key markets globally, where acquiring our distributors might make sense. Our Australia acquisition from last year that I mentioned a second ago, is a great example of this, where we have 3x the revenue we had prior to the acquisition, highest margin profile in the system, and we can directly execute on all facets of the go-to-market in country. As we've discussed before, the closer we are to the end customer, the more successful we are in that particular market as product awareness propagates. Secondly, we're looking into the channel for things like dealership services, where we can invest in a part of the market that we don't think is well served to tie into my remarks earlier. And finally, we'll always look at adjacent product or service lines that complement our current portfolio as a possible acquisition target. One example of an adjacent market is colored films.”

- Ryan Pape, CEO, Q3 2023 Earnings Conference Call

“So we'll continue with the smaller acquisitions. We're also looking at some larger acquisitions, larger for us in a relative sense, $25 million to $50 million plus purchase price. This could have a more significant impact on the business, bring on new markets or capability or scale. So even though our average acquisition size has been quite a bit smaller, we're very much open to incrementally larger acquisitions and these would have an impact on the business, but they don't change who we are. They're not transformative in a sense that it turns us into something we don't want to be, but very active on that.”

- Ryan Pape, CEO, Q4 2023 Earnings Conference Call

Xpel has successfully integrated new film suppliers into its supply chain. This process resulted in a few hiccups in 2023, including some small inventory write-offs and one-time RnD expenses, but these are now behind the company. In addition to decreasing risk from a single supplier, a goal of the company for several years now, this has also already allowed Xpel to expand its product offerings. Xpel recently revealed brand new Windshield Protection Film, Marine PPF, rebranded wash/prep products, and several new architectural films at XDC24 (Xpel Dealer Conference 2024). I’m optimistic we will see colored PPF options in the future, which, in my opinion, has the potential to disrupt the $7 billion 20% CAGR growth vinyl wrap industry.

The upcoming launch of Xpel’s e-commerce website (maybe later in 2024) has considerable potential implications and opens Xpel up to higher margin B2C sales, a brand new channel and TAM. It seems market participants have completely forgotten about this, as I have not seen this mentioned anywhere else.

And then additionally, we have a new global platform launching next year, a global web platform launching next year with enhanced e-commerce for selling car care products to increase the number of touch points we have with our customers over the lifetime ownership of their vehicle.

- Ryan Pape, CEO, Q3 2023 Earnings Conference Call

Insider sales have completely halted since October 2023. Although this is highly speculative, I believe this is because insiders are confident in the business and now believe the business is undervalued. Insiders have not sold one single share since the Culper Research short report in October. If the Culper report had any merit, Insiders would undoubtedly be rushing to dump stock. That is not the case here.

The short reports from late last year make numerous glaringly obvious and shameless mistakes, including but not limited to:

Shorts are incorrectly comparing Xpel’s Paint Protection Film to Vinyl Film. These are, in fact, completely different products with different purposes and use cases, and can even be paired together (meaning not only is Vinyl NOT a threat, but it can benefit Xpel as the market demand for Vinyl grows). PPF can be installed over Vinyl film to protect the Vinyl film (this currently is rare, but has the potential to become more common). Furthermore, installers are highly incentivized to upsell from cheap low-margin vinyl film to expensive high-margin paint protection film.

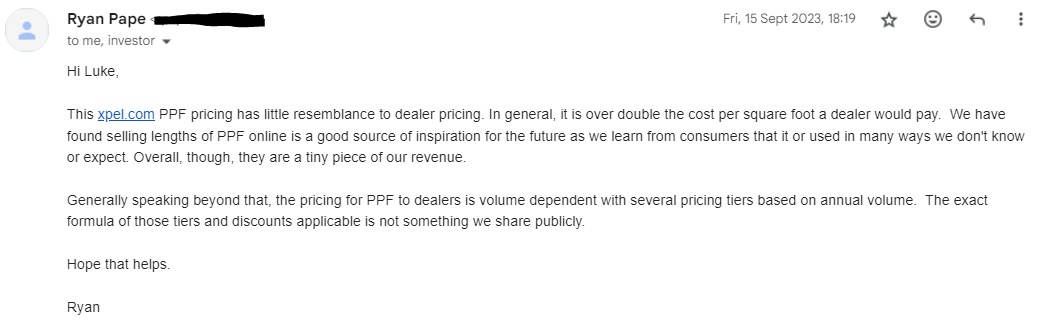

Overstating Xpel’s cost of film/pricing by close to 100%, thereby causing investors to falsely believe Xpel’s film is not competitively priced, and greatly misrepresenting Xpel’s current pricing model. I’m going to take an optimistic view here and say the VIC short seller is simply incompetent.

I confirmed with CEO Ryan Pape that Xpel’s website pricing is not indicative of the pricing installers get. Xpel uses a tiered pricing system based on volume for installers, and it can be approximately half the price shown on the website. Ryan Pape told me they have film available on the website as it will occasionally be ordered for new use cases that Xpel did not think of, thereby giving Xpel new ideas for new and existing product lines. But he made it clear, this is NOT the pricing installers get.

The image below shows these points exactly. This image is from the VIC short writeup, whereby the author took the Xpel website price for 5x15 PPF, and compared it to other brands at their wholesale/installer prices. In reality, Xpel’s film is extremely competitive on price with other brands at less than half of what is shown in the VIC writeup. Furthermore, the HOHOFILM pricing here is for Vinyl Wrap, not PPF. If you search specifically for HOHOFILM PPF you will find their 5x15 rolls of PPF are priced closer $250-400, with 2 week+ shipping times to North America (such shipping times are completely unfeasible for North American installers).

Shorts are making erroneous claims that Xpel’s films are obsolete due to supposed paint technologies from Xpel’s main supplier, Entrotech. We now know these claims were completely fabricated out of thin air and were predicated on creating an environment designed to scare shareholders into panic-selling and driving the stock price lower. As it turns out, Ford recently announced their product offering in partnership with PPG & Entrotech on Mustangs, and it is nothing more than regular paint protection film. While this does increase competition, it certainly is not some new technology rendering Xpel’s films obsolete.

Shorts have greatly exaggerated the degree to which Teslas contribute to Xpel’s business.

Shorts failed to mention or recognize Xpel’s wholesale business, absolutely none of which is from Tesla.

I recently posted a comment on the recent Scuttleblurb writeup on Xpel explaining these two points in further detail:

Shorts have greatly exaggerated the degree to which Tesla offering its own films serves as a competitive threat to Xpel. There is strong evidence to suggest this will benefit the global market leader in PPF (Xpel). Numerous case studies illustrate this phenomenon including some of the world’s biggest businesses like Netflix, and Apple. Furthermore, evidence already suggests that Tesla’s film installation is of lower quality and that they’re not investing correctly (I believe due to incapability) to make it a value-added service competitive with third-party Xpel or Suntek/Llumar installers.

Shorts are greatly exaggerating the degree to which Xpel film has been given away for free by dealers. This is a claim made in the VIC short writeup. My investigation found absolutely zero evidence of this ever occurring, though I cannot say for sure. It is far more likely that PPF prices have been negotiated down through standard vehicle purchase negotiations, and shorts have taken this to mean that PPF is included for free, which is not the case. In further emails with Xpel CEO Ryan Pape, he reassured me that this is not a common practice or something that ever really happens in the industry.

Ultimately my numbers for Xpel this year are as follows:

I’m forecasting Sales of $455M in 2024, with EPS coming in at $2.26 as my base case. My bull case has sales of $475M and EPS of $2.64.

I estimate that Xpel could achieve $5.00 of EPS by 2027 (22% EPS CAGR from estimated 2024 base case), resulting in a minimum multiple of 20X and a stock price of $100 per share (17% CAGR from $54 per share today), or a maximum multiple of 30X, and a stock price of $150 (29% CAGR). In short, there is a clear path for 4-year annual returns approaching ~20-30%. Using a reasonable discount rate of 12% from a mid-point price of $125 in 4 years, fair value today would be $79.40. Using a future price of $150 and the same discount rate would result in a fair value of $95.30 today. Furthermore, one could argue this discount rate is too high in the current market environment, which is currently pricing in ~5-7% fwd returns for the S&P500.

Disclosure: I’m long XPEL.

Disclaimer: This post and all Uncommon Profit posts are not financial advice in any way and should not be taken as such. All articles, including this one, and all information within Uncommon Profits are for educational and informational purposes only. I receive no direct compensation from any company covered. I will likely profit in the event the share price of companies covered increases and I have a long position. I will likely profit in the event the share price of companies covered decreases and I have a short position. Although I make an effort to update readers when possible, I may choose to buy or sell at any time with no obligation to update or notify readers. Consult a professional financial advisor before making any investment decisions.

Thumbnail Image courtesy of Harrison Haines

This newsletter is currently free. If you’d still like to support it financially, you can Buy Me A Coffee as a one-time tip here (USD):

Fantastic level of detail!

Now, if we zoom out, how do you look at the risk that, one day, car manufacturers have a competitive PPF offering (bear case valuation)?

XPEL drops 32% after Q1 earning. Any thought? China impact?